How IEX non-displayed midpoint trading has increased on the back of a tripling in displayed market share.

As many of you know, IEX has seen a surge in Displayed Trading since introducing new pricing tiers to compete with other large exchanges, growing our displayed market share by about 3x since June.

What many might not realize is that IEX midpoint market share has grown as well over that timeframe. As the saying goes, “liquidity begets liquidity.” and IEX has expanded its exchange midpoint intraday market share in single stocks by 20% from earlier this year. As we discussed in a recent blog, this growth has come without any degradation whatsoever in midpoint fill quality, if anything midpoint markouts are better than ever.

More specifically, IEX now has now has the largest midpoint market share in single stocks compared to all other exchanges with Nasdaq a close second (with lower execution quality).

Since its inception as an ATS, IEX has been known as a venue where traders can rest large hidden orders at the midpoint due to the structural protections of the speed bump. These protections were further enhanced with the Signal and the D-Peg order type. Despite average fill size marketwide continuing to decline, we can see in the below chart that IEX actually has more than 50% market share of midpoint block trades which occur on-exchange, and that figure has actually grown in recent months. While some traders may think of ATSs as the primary source of midpoint block trades, IEX’s position as an exchange represents a unique opportunity. ATS trades are not “attributable” to the tape following an execution, meaning traders don’t know which ATS or other off-exchange venue a block trade occurred on unless they were a party to the trade. As an exchange, IEX’s trades are attributable to the tape, allowing traders to use “heat maps” to direct flow towards IEX following a large block trade in a stock on IEX.

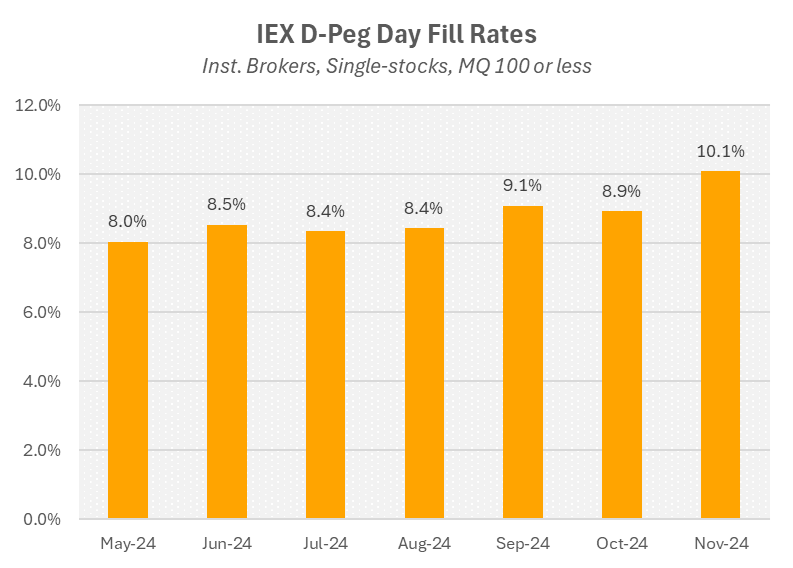

Given this growth in midpoint market share, it may come as no surprise that the fill rates of institutional brokers using D-Peg, IEX’s flagship midpoint order type, have also increased by 18% since May, adding to the attractiveness of using D-Peg.

As we have written about before, IEX market share peaks between 3:58 and 3:59pm. That market share increase comes from both lit and dark trading, and that dark trading in particular stands out against falling off-exchange volume (where most dark trading occurs throughout the day). Taking a look at D-Peg hit rates by time of day, we see that they are more than double in the final minutes as compared to the rest of the day.

While IEX’s recent growth in displayed trading has rightfully garnered a lot of attention, we think IEX’s non-displayed trading should get just as much consideration, especially given the significant rise in off-exchange trading (where, at times, higher market share comes with lower execution quality).

On exchange, where public data allows for more fulsome comparisons, IEX continues to be a proven and unique source of quality midpoint and block trading, and our market share growth in recent months is a testament to that. Finally, IEX can be particularly potent for mid-point trading in the final minutes of the day so please ensure that your strategies are optimized to source liquidity from IEX during this time of day as well.

Please don’t hesitate to reach out to sales@iextrading.com to learn more about how to optimize for IEX’s unique dark liquidity.

Head of Business Analytics